Research plays an important role in shaping today’s technological and innovative world—whether in medicine, technology, or other areas of advancement. Our government recognizes that progress depends on research and that its benefits extend to everyone. To encourage innovation, it offers a tax credit to businesses through IRS Form 6765, titled “Credit for Increasing Research Activities.”

However, not every research activities qualify for this tax credit. So, to understand which activities are eligible, how to file, and what rules and regulations apply, continue reading this post. Herein, you can discover everything you need to know to successfully claim the tax credit for research activities.

Herein, we have provided you with all the new changes that are included within Form 6765.

According to the latest updates, the reduced credit election under section 280C is now done at the top of the Form 6765 on Item A. Mark the Yes option to elect and No for not electing the section 280C reduced credit on your timely filed return, consisting of the extensions.

Item B in the form prompts you whether you are a member of a controlled group or business under common control. Also, you need an attachment of the Form 6765 if you have marked the Yes option.

For reporting the Qualified Research Expenses (QREs) on line 48, fill out Section E.

If you are eligible to file Form 6765 and select to follow this directive, hit the Yes tab on line 41.

This section usually reflects whether it’s necessary to complete Section G. Then, insert your total QREs on each applicable line.

For the taxation years starting before 2025, Section G will be optional for all filers. In case you are filing an amended return, then file the Research Credit Claims on Amended Returns.

For those lines that provide an attachment, access the naming convention explained in the Specific Instructions section if you e-file.

The IRS Form 6765 is used to figure out and claim the credit for increasing research activities. Also, it’s used for electing the reduced credit under Section 280C and for electing to claim the specific amount of credit as a payroll tax credit against the employer.

This form is to be filed by the Partnerships and S Corporations to get the claim on the credit. Other industries aren’t required to file this form if their only source for their credit is a partnership, S corporation, estate, or trust. Despite this, they can report their credit directly on the Form 3800. Furthermore, if you are a trust or an estate, then the credit can be assigned to the beneficiaries.

The Form 6765 is basically used to:

Figure out and then claim the credit for increasing research activities.

Elect and for figuring out the payroll tax credit.

Also, it is used to elect the reduced credit under section 280C.

Proper documentation is required to claim the R&D payroll tax credit. Herein, we have discussed all of them in detail.

Firstly, you must specify the purpose of the research activity, whether you are claiming to enhance the performance, reliability, functionality, or the quality of the product.

Also, you must provide the schematics, technical requirements, and blueprints.

Moreover, you must also process the flow diagrams.

To qualify for the R&D payroll tax credit, a business must meet the following requirements.

The maximum amount to claim for the R&D payroll tax credit for small businesses against payroll liability is $500,000.

In case you are claiming a refund or credit on an amended return, which consists of a section 41 credit for increasing research activities, you have to offer certain information so that your claim is marked as valid.

To file Form 6765 with the IRS, you must implement the steps instructed below.

Pro Tip: If you’re a small business or startup looking for a step-by-step walthrough, check out our detailed guide on filing IRS Form 6765

Access the four IRS forms to detect whether your research activities qualify for the R&D tax credit. Make sure that it might consist of a technical uncertainty, also be scientific in nature, and generate a permitted business component. Also, make sure that you include an experimentation process.

Now, begin adding your qualified research expenses (QREs), that is, basically the costs incurred in your research activities and the basis for your credit amount. It might comprise:

Wages-

Herein, you can add any wages that include bonuses and stock options. Also, it includes redemptions paid to in-house employees for qualified services like directly engaging in, supervising, or supporting qualified research.

Supplies-

Herein, insert the cost of any tangible property used to complete the qualified services. Make sure that you include the cost of those properties which is depreciable.

Contract Research Expenses-

Herein, mention the 65% of any expense paid to a person who isn’t an employee. The cost is incurred on the activities which is considered as qualified services or research if done in-house.

The Section 280C election affects how you have claimed the startup R&D tax credit. Moreover, you can make the election on a timely tax return, which won’t allow you to file the Form 6765 again along with an amended return.

Without the election, it won’t be possible to claim the full amount of your credit. But, herein, you can include the amount back into your taxable income. Moreover, with the election, you must reduce your credit by the corporate tax rate by 21%. But you can’t include this credit in your income.

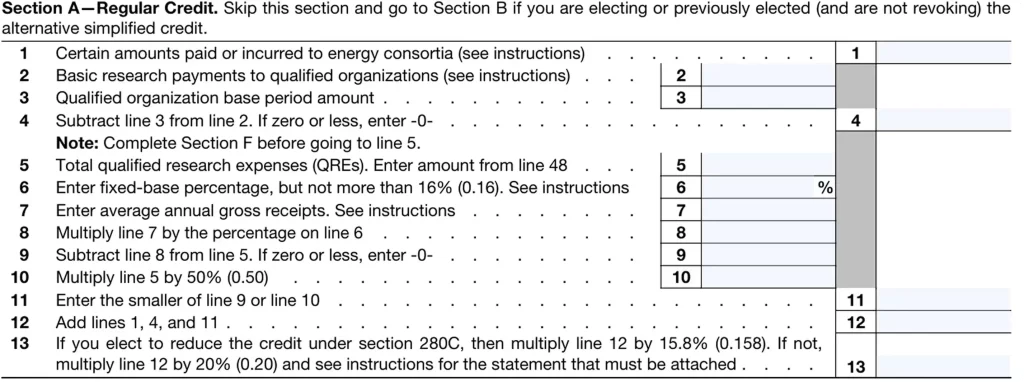

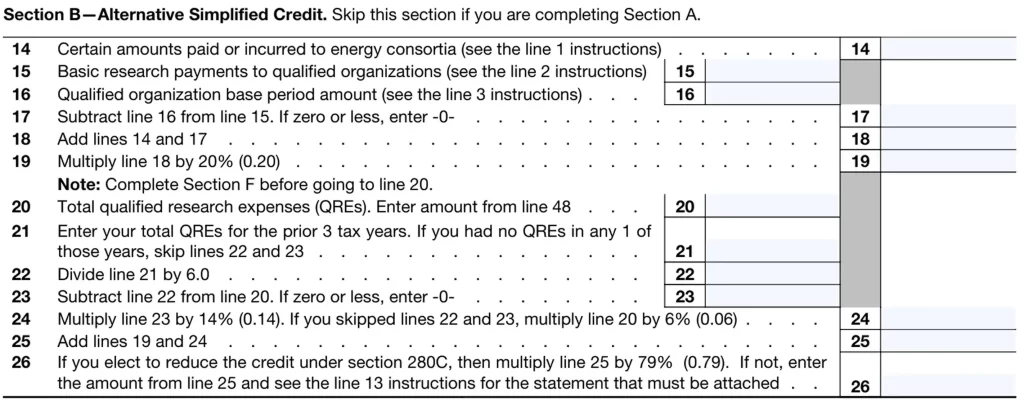

Now, you can compute the R&D tax credit with the help of the regular method or the Alternative Simplified Credit (ASC). Usually, this method is necessary to compute your credit using both and then select the higher amount.

With the help of the regular method, you can compute your credit as 20% of the difference between the current year QREs and an amount based on historical R&D spending. This amount is best for businesses with a long history of consistent r&D spending.

Whereas, the ASC method is used to compute the credit as 14% of the difference between current year QREs and 50% of the average QREs from the last three years. In case you have any QREs from the last three years, then it’s computed as 6% of the current year’s QREs.

In case your business is qualified as a small business (QSB), then you can elect to apply for the portion of your R&D credit up to $500K against the payroll taxes. For qualifying as a QSB, your company must require:

The five years of gross receipts

Your company must have less than $5 million in gross receipts for the current year.

Herein, you can use Section C to provide detailed insights into the current year’s credit, including the portion attributable to different entity types.

The Section E prompts you to add essential details, including the number of business components that create QREs. In the meantime, Section F needs a summary of your QREs, and you can access Section G for the growth of your business component information.

Looking for a step-by-step guide on business tax filings beyond Form 6765: Check out our complete Tax Guide for Small Businesses

With this, we conclude this post and hope that you can now easily file the Form 6765 with the IRS. Also, you come to know about the businesses that qualify to file this form.

Furthermore, to gather more details regarding the R&D credit payroll form, you must connect with our BooksMerge experts. You can connect with the professionals through the live chat or by placing a call for immediate resolution.

Before you start filing this seaso, make sure you understand all essential IRS documents: Read our guide on the Top 10 IRS forms for Beginners in 2025

The businesses claiming the R&D Tax credits have a time limit of up to two years after the end of the accounting period.

Any company that is involved in activities to develop or improve products, processes, software, formulae, or inventions that need some level of technical experimentation. This is basically required to determine the appropriate design that is eligible for the R&D credit.

The Startup taxpayers may claim up to $500,000 of their FICA for up to 5 years with the help of R&D credits.

If you are investing in innovation, then you qualify to make an R&D tax credit for obtaining either a cash payment or a Corporation Tax reduction.

To claim the R&D tax credit, you must have the following:

Tax and payroll records

Testing documents that include project records, lab notes, design drawings, prototypes, and patent applications.

A report that is used for tracking time, expenses, and other project account details.

The companies that are eligible to claim the R&D tax credit include Technology companies, pharmaceutical companies, engineering businesses, and manufacturers.

The IRS allows you to revoke an Alternative Simplified Credit (ASC) election only for a future tax year. To do so, complete Section A (Regular Credit) instead of Section B (Alternative Simplified Credit) on a timely filed original Form 6765.

A Form 6765 preparation service Orem UT may be beneficial for businesses that perform qualified research activities, including manufacturers, software developers, engineering firms, construction companies, and other businesses that may qualify for the federal Research Credit.

AI-triaged.

Human-solved.

Instant QuickBooks diagnostics, then a certified ProAdvisor takes over live.

first-call fix

match time

live coverage